Author: Tim Sharp

Researcher: Jack Williams

Published: November 21, 2023

Millions more around the U.K will be paying more in tax come the new year as Jeremy Hunt, the latest appointed chancellor, tries his hand in taming inflation and calming the markets with his Autumn Statement.

On Thursday morning, Chancellor Jeremy Hunt embarked upon £55Bn of savings as he cuts public spending and attempts to raise funds through a round of “stealth” taxes that will likely affect millions the length and breadth of the United Kingdom.

Independent forecasts from the Office for Budget Responsibility (OBR) have revealed that the statement will see Britain face the biggest hit to living standards on record, with £30Bn of delayed spending cuts and £25Bn in backdated tax increases.

The announcement comes after inflation hit a new 41-month high, reaching 11.1% in the middle of the U.K.’s cost of living crisis.

While no one seems to be safe from the Chancellor’s sweeping plans, which touch everything from dividends to defence spending, many families and investors are probably wondering what this means for the markets, their finances and their families.

Key Announcements

45p Tax Rate

The 45% top rate of tax, recently poised to be scrapped by Truss’ government has been reinstated, while the threshold has been lowered from £150,000 to £125,140. This means those earning £150,000 or more will now pay around £1200 more per annum in tax.

Income allowance, National Insurance and Inheritance Tax

The Conservatives announced a freeze on income tax personal allowances, national insurance and inheritance tax until April 2028, while benefits and state pensions are set to rise in line with inflation.

Windfall Taxes

The government has pulled a 180-degree U-turn on its prior stance of opposing the uprating of the tax upon oil and gas producers’ excess profits, increasing the levy from 25% to 35% while imposing a further 45% rate on energy generators making “extraordinary profits”. This affects businesses where electricity is being sold above 1.5x the average 10Y electricity price, meaning a headline rate for affected businesses of 70% once corporation tax is factored into account.

Nuclear Energy

The Government has confirmed its plans for the Sizewell-C nuclear plant, calling Britain “a global leader in renewable energy” in the Chancellor’s statement. Hunt also spoke about furthering the green agenda, pointing towards offshore wind and carbon capture as future areas to explore while promoting nuclear as the solution to the U.K.’s energy mix.

Dividend Allowance

The past five years have seen a dividend allowance of £2000 in place, down from the prior £5000, which has now been halved from 2023 to just £1000, and from 2024 halves again to just £500. Although this is on top of the £12,500 personal income allowance which everyone gets, from 2024 it will be just 10% of where the allowance stood in April 2018.

Capital Gains Tax Allowance

Jeremy Hunt has decided to increase the tax on growth as well as income for investors by halving the current capital gains tax allowance from £12,000 to £6000 from April 2023, before being slashed again by 50% in 2024/25 to a £3000 p.a. allowance.

- The Chancellors statement has resulted in a United Kingdom with the highest tax burden since records began.

- On only three occasions in history have disposable incomes fallen, in real terms, for two consecutive years as they have over the past 24 months in the U.K.

- The economic decline is expected to return living standards back down to 2013/14 levels, with current rates not being recovered for an estimated six years.

What does this mean for U.K. investors and what can you do?

Investors in the U.K will likely see a notable difference coming into the new year from the governments statement on Thursday. Forecasts from the Institute for Fiscal Studies (IFS) identified middle income families to be the worst affected with the typical U.K household taking a permanent 3.7% income hit.

However, by utilising different strategies, investors may be able to mitigate some of the negative impacts from Jeremy Hunt’s statement last week.

Combining Capital Gains Tax (CGT) Allowances

Couples are reminded that, if married or in a civil partnership, they can combine their CGT allowance. Couples where only one of them is using their CGT allowance can merge with their partner to ensure maximum use of the lowered thresholds.

Using an ISA

ISAs offer an annual tax-free allowance of £20,000 and may be considered one of the most efficient ways to mitigate tax on investments. However, liquidating a portfolio to fund an ISA may trigger CGT if the gain is above the CGT allowance.

Start Ups to Mitigate Tax Impacts

Investing in start-ups, when done efficiently, might also mitigate some of the impact of the Chancellors statement.

Venture Capital Trusts (VCT’s) invest in emerging British businesses and offer a number of tax reliefs such as 30% upfront income tax relief, tax-free dividends, and an exception from capital gains tax on shares should they rise in value, provided they are held for a minimum qualifying period.

Enterprise Investment Scheme

The Enterprise Investment Scheme (EIS) is a governmental incentive that provides a source of funding to early-stage U.K companies while offering tax benefits to holders.

EIS is seen as one of the most tax-advantaged of government schemes, with opportunities to mitigate income tax, capital gains tax and inheritance tax; designed to support growth-focused, early-stage and unquoted companies to raise funding they may have otherwise struggled to attract due to their early stage and therefore higher risk status.

While early stage ventures come with a higher risk and growth potential, EIS can offer relief to investors in the form of tax and loss benefits such as income tax relief (Investors can claim up to 30%, £1m maximum p/a for a maximum of £300,000 worth of income relief), tax free growth (any growth in an EIS investment is 100% tax free), capital gains deferrals (a gain made on the sale of other assets can be reinvested in EIS and differed over the life of the investment) and loss relief (ability to offset the loss on an EIS investment against their Capital Gains or Income Tax).

Summary

While moves aimed at pushing the U.K back towards sustainable finances may be fit for the job at hand, the Bank of England, OBR, and government forecasters all agree that the U.K is now on the brink of a recession, with the normal counterbalance of fiscal stimulus remaining firmly off the table.

The question is, how do U.K investors protect themselves against a recessionary environment? There is no single solution, however while Hottinger does not offer tax advice, there are schemes, incentives, and avenues of opportunities available that may make the most of current allowances and bolster one’s finances looking forward depending on each investor’s risk tolerance.

https://commonslibrary.parliament.uk/research-briefings/cbp-9643/

https://www.bloomberg.com/news/articles/2022-11-18/uk-s-middle-income-households-squeezed-hardest-by-fiscal-plan

https://ifamagazine.com/article/autumn-statement-reaction-from-investment-and-financial-experts-to-chancellor-hunts-announcments/

https://www.gov.uk/guidance/venture-capital-schemes-tax-relief-for-investors

https://www.gov.uk/guidance/venture-capital-schemes-apply-for-the-enterprise-investment-scheme

https://www.gov.uk/government/publications/enterprise-investment-scheme-and-capital-gains-tax-hs297-self-assessment-helpsheet/hs297-enterprise-investment-scheme-and-capital-gains-tax-2019

https://www.syndicateroom.com/eis#:~:text=No%20tax%20on%20EIS%20gains,must%20already%20have%20been%20claimed.

https://www.bbc.co.uk/news/uk-england-suffolk-63664140

https://www.theguardian.com/uk-news/2022/nov/17/biggest-hit-to-living-standards-on-record-as-jeremy-hunt-lays-out-autumn-statement

https://www.theguardian.com/politics/live/2022/nov/17/autumn-statement-2022-live-jeremy-hunt-to-unveil-budget-plans-as-labour-says-12-years-of-tory-economic-failure-holding-uk-back-rishi-sunak-latest-updates

https://www.ft.com/content/8af720e0-1946-4c42-8dcb-ee6ea679bbb6

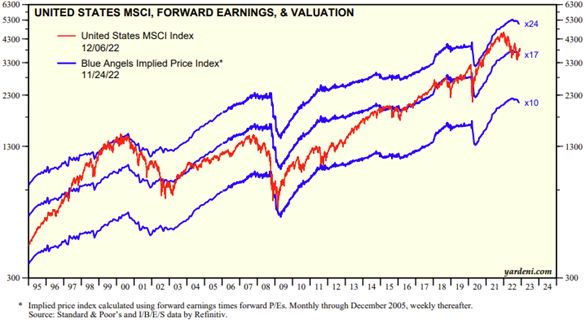

Source: Hottinger Investment Management / Refinitiv Datastream

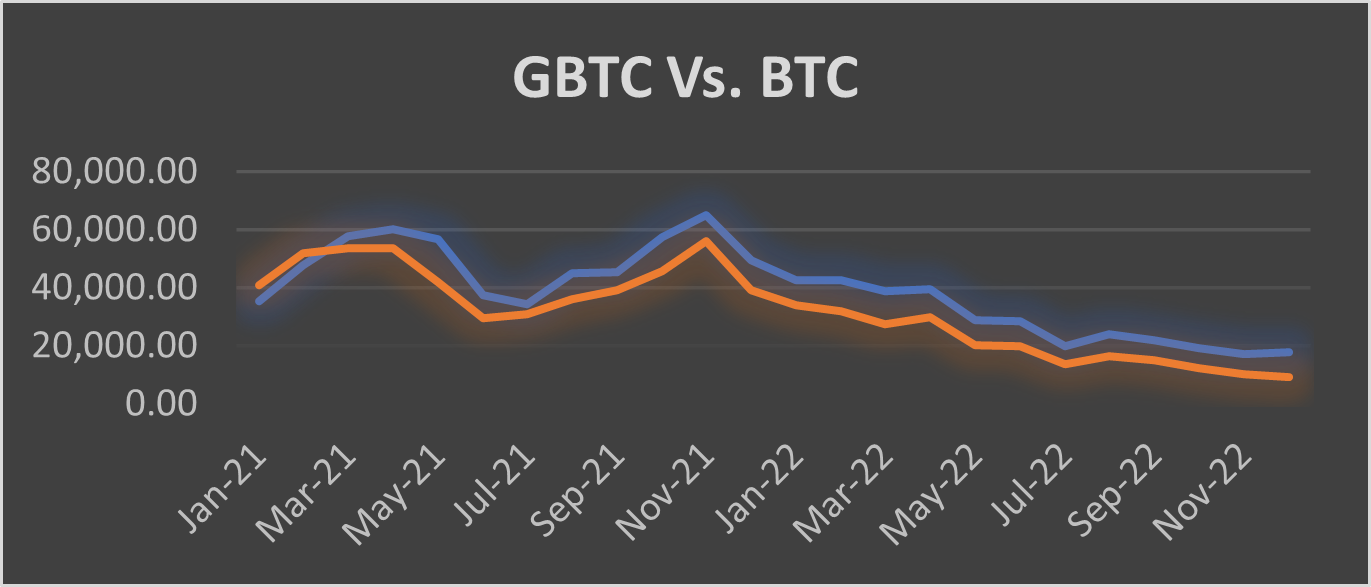

Source: Hottinger Investment Management / Refinitiv Datastream

Source: Hottinger Investment Management / Refinitiv Datastream

Source: Hottinger Investment Management / Refinitiv Datastream